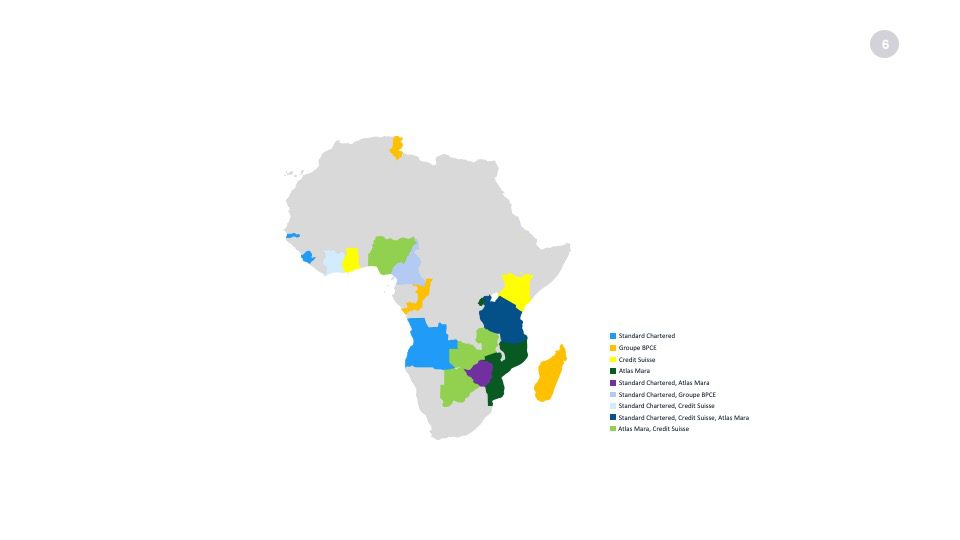

On 14 April 2022, the UK-regulated emerging markets bank, Standard Chartered Plc, announced plans to fully exit five markets in Africa (Angola, Cameroon, Gambia, Sierra Leone, and Zimbabwe) and will only retain corporate banking in Côte d’Ivoire and Tanzania. The bank, which once prided itself on the fact that it has been operating in Africa for more than a century, is abandoning its ‘here for good’ brand promise. Standard Chartered has been operating in Zimbabwe since 1892 and the former breadbasket of Africa was the bank’s fifth highest revenue generator globally as recently as in 2004. The bank’s Sierra Leone and Gambia offices opened in 1894; Cameroon in 1915; and Angola in 2014. Across many of the 15 markets where it operates, Standard Chartered is the oldest financial institution and has been steadfast in its unwavering support to the local economies. Until now.

Book recommendation Crossing continents: A history of Standard Chartered Bank by Duncan Campbell-Smith. £24.99 (hard cover), £14.99 (kindle). Available on Amazon using the link above.

The Standard Chartered press release stated that the impacted markets accounted for “around one percent of total Group 2021 income” and that the bank would continue to serve corporate clients in those markets, presumably from regional hubs in South Africa, Kenya, and Nigeria. As of early this week, it was unclear to some impacted staff and clients exactly how and when this transition will happen.

Hong Kong-based Citi equity analyst, Yafei Tian, provided Reuters with the following explanation for the exits: “… the complexity of operating at that scale left the bank with a comparatively high cost-to-income (COI) ratio of 74%, which exiting sub-scale markets will help to improve.” It would be good to understand from Ms Tian how exiting markets where the average banker earns $350-2,000 per month will make a difference to the group’s high COI. The real culprits for the high COI are the bloated management layers in London, Singapore, Hong Kong, and Dubai.

Standard Chartered is not the first long-standing international bank to partially bid the continent adieu. In February 2022, the scandal-prone Credit Suisse exited its wealth management businesses in Botswana, Côte d’Ivoire, Ghana, Kenya, Mauritius, Nigeria, Seychelles, Tanzania, and Zambia. It will only maintain a presence in South Africa and will refer clients to Barclays. Barclays Plc also exited Africa in 2017 when the UK bank sold its majority stake in Barclays Africa Group Limited (BAGL), which has since rebranded itself as Aba Group. Barclays had been in Africa since 1925 and made a strategic decision to focus on core markets in the UK and the United States. Similarly, the French banking group, Groupe BPCE exited non-core businesses in Cameroon, Madagascar, Republic of Congo, and Tunisia in September 2018.

New entrants to Africa are pulling the plug even quicker. In October 2021, Atlas Mara withdrew from seven markets in Africa: Botswana, Mozambique, Nigeria, Rwanda, Tanzania, Zambia, and Zimbabwe. It found the macroeconomic environment challenging and the risks far outweighed the reward. The bank quit just seven years after boldly stating that Africa was “too big to ignore” and its ambition was “to be a positive disruptive force in Sub-Saharan Africa.”

The biggest challenge for African regulators when foreign banks exit is to ensure that there are correspondent banking arrangements in place to support cross-border remittances, payments, and trade finance. Increasing regulation and compliance costs have made correspondent banking less appealing for many international banks. Deutsche Bank stopped clearing US dollars for Stanbic Zimbabwe in August 2021 because of heightened sanctions risks. Stanbic Zimbabwe will now rely on nested banking arrangement via its parent, Standard Bank, which will increase the cost of doing business. Many local banks will struggle to do cross border transactions.

Africa could learn from the Caribbean, which is still recovering after massive de-risking of correspondent banking relationships from 2015 crippled remittances, trade, foreign direct investments and increased transaction costs for consumers. Regulators in the island nations have worked so hard to remediate that they have surpassed Africa, which is now at the bottom of the Basel AML Index 2021.

The 2021 Basel AML report specifically called out Cape Verde, Democratic Republic of Congo, Mali, Mauritania, Mozambique, and Uganda as having “zero effectiveness in both the prevention and enforcement” of AML. These are early warning signs about the increasing risks and compliance costs for foreign banks, which coupled with falling profitability, will trigger more exits from Africa unless Central Banks in the region take urgent action.

The upcoming African Development Bank (AfDB) Annual Meeting to be held from 23-27 May 2022 is the biggest gathering of all the continent’s Central Bank Governors and the banks that operate in the region. The issue of foreign bank exits, correspondent banking de-risking and failing AML regimes will need to be addressed with the utmost urgency.

Many people think that foreign banks are exiting Africa because there is no money to be made, which could not be further from the truth. Foreign banks are replacing a physical presence with a suitcase banking model that allows them to periodically fly in and out of a country while maintaining the most lucrative accounts. Assets linked to these accounts and the associated revenue are probably already booked offshore. It is important to understand that published financial statements by local subsidiaries of foreign banks in Africa do not give a true picture of the value the foreign bank is deriving from that markets. Read this point again.

| Top 10 deals in Africa (2020-2021) and the local/ Africa regional/foreign banks involved |

| Mozambique LNG USD 14.9bn Commercial and ECA-Backed Term Loan (July 2020). Regional banks: Absa, AfDB, AFREXIM, IDC, Nedbank, Rand Merchant Bank, Standard Bank Foreign banks: ICBC, SMBC, Societe Generale, Cassa Depositi e Prestiti, Credit Agricole, DBS Bank, JPMorgan, Mizuho, MUFG, Nippon Life Insurance, Shinsei Bank, Standard Chartered, Export-Import Bank of Thailand, US EXIM, JBIC, UKEF |

| Republic of Ghana USD 3.25bn 144a/RegS 4-Tranche Bond (April 2021) Local banks: CalBank, Fidelity Bank Regional banks: Rand Merchant Bank, Standard Bank Foreign banks: Citi, BofA Securities, Standard Chartered |

| African Development Bank USD 3.1bn 144a/RegS Social Bond (April 2020) Foreign banks: BofA Securities, Citi, Credit Agricole, Goldman Sachs, TD Securities |

| Ministry of Finance and Planning, United Republic of Tanzania USD 1.641bn Syndicated Commercial and ECA-Backed Term Loan (June 2020) Regional banks: AFREXIM, DBSA, TDB Foreign banks: Standard Chartered, KfW-IPEX Bank |

| Bank of Industry USD 1bn Syndicated Term Loan Facility (Dec 2020) Regional banks: Africa Finance Corporation, AFREXIM, Rand Merchant Bank Foreign banks: Credit Suisse, SMBC |

| Ministry of Finance, Republic of Angola USD 910m Syndicated Loan/IBRD Partial Risk Guarantee Facility with ATI CRI Cover (June 2021) Foreign banks: Standard Chartered Bank, BNP Paribas, Credit Agricole, Credit Suisse, Societe Generale, Landesbank Hessen-Thüringen, Santander, World Bank, BPI |

| African Export Import Bank (AFREXIM) USD 907.5m Loan (May 2020) Foreign banks: EmiratesNBD, MUFG, Standard Chartered, Bank ABC, HSBC, State Bank of India, ICBC, Mizuho, Rand Merchant Bank, SMBC, Commerzbank, First Abu Dhabi Bank |

| Helios Towers USD 750m 144a/RegS Senior Unsecured Bond (June 2020) Regional banks: Absa, Standard Bank Foreign banks: BofA Securities, JPMorgan, Barclays |

| Africa Finance Corporation USD 700m RegS Senior Unsecured Bond (June 2020) Foreign banks: JPMorgan, MUFG, BofA Securities, Goldman Sachs |

| Access Bank USD 500m 144a/RegS Perpetual NC5.25 Bond (Sept 2021) Local banks: Coronation Merchant Bank Foreign banks: Citi, JPMorgan, Mashreq, Renaissance |

What is frustrating is that African pension funds and central banks, the custodians of the local banking systems, are the very clients that are managed by suitcase bankers. JP Morgan has been managing a sizeable proportion of Central Bank of Nigeria (CBN) reserves since April 2006 and earns an guestimated 8-9 figure USD fee annually - though this position has gradually reduced in recent years with leading Nigerian banks being given more responsibility for reserves management. The arrangement continued even after JP Morgan dropped Nigeria from the Emerging Markets bond index in 2016 and CBN is currently suing JP Morgan for $1.7bn for allegedly making a fraudulent payment of $875m back in 2011. Nigeria’s forgiving nature is in sharp contrast to Saudi Arabia’s handling of Citi which exited the Kingdom immediately after 9/11 and spent 20 years begging to be let back in after the rulers repeatedly snubbed them.

The question to African regulators is why are we willingly giving away our crown jewels to foreign banks who do not value Africa? Respect and loyalty should be non-negotiable principles when doing business.

The regulations that are driving some of the exits and which have had the greatest impact on the banking system in Africa are issued by the Financial Action Task Force (FATF), which is the global money laundering and terrorist financing watchdog. FATF was founded by G7 countries in 1989 and has 39 members.

South Africa is the sole representative for the continent and has a mature banking system that bears more similarities to Western markets than to other African countries. It would be ideal if FATF membership could expand to include countries such as Nigeria, Kenya, and Egypt so that the voice of less mature banking systems is heard. The rest of Africa is currently represented by Associate Member bodies whose role is to implement FATF recommendations rather than input, debate, and challenge decisions.

International banks have struggled in Africa because they impose Western banking standards and products instead of trying to understand and meet the needs of the market. Unfortunately, this problem is compounded by the fact that many local banks, which emerged long after international banks, have copy-and-pasted the same approach and Central Banks have an attitude of deference to the West.

The Western approach to Know Your Customer (KYC) requires formal identification documentation (national IDs or passport), proof of address (utility bill, mortgage agreement, or bank statements) and proof of income (payslips or bank statements). KYC is one reason why most Africans remain outside the banking system: an estimated 500m people on the continent do not have IDs; the lack of urban planning has resulted in residences, built from own savings, sometimes without street names and numbers, and providing their own utilities; and most people are informally employed and unable to prove how they make a living. These are just the barriers to opening an account – the bar is even higher when trying to get credit.

As a result, the financial services landscape in Africa is highly fragmented with traditional banks serving the small formal sector while fintechs, mobile money and micro-lenders serve the much larger informal sector, which is as much as 80% in some countries. The informal sector is where the innovation is happening. In Somalia, where Barclays and other international banks ended correspondent banking relationships in 2015, it is the Fintechs that are supporting aid agencies like World Vision and Save the Children to move funds by compensating for the lack of national IDs by using referrals from clan networks and the use of biometrics.

African Central Banks should have tabled these challenges and proposed alternative solutions to bodies like FATF, to gain universal acceptance. Instead, we’re seeing European banks like HSBC launching products called ‘No fixed address bank account’ to cater for the homeless, which is solves for similar issues that have been bouncing around unresolved for decades in Africa. We just don’t help ourselves.

Local and regional banks have a key role to play in finding innovative solutions because there are limitations to what fintechs and mobile money operators can do, such as facilitating cross-border trade. The less stringent regulations outside the banking sector is also driving up the AML risks in the region, which should be of great concern given the negative consequences previously highlighted.

Africa needs to remain part of the global financial system and as more international banks retreat to their backyards, it is imperative that local and regional banks start playing a leading role in the sector.

It is only African banks that we can be certain will be here for good.

Brilliant article Muloongo! I hope to see other banks really step up and grab the opportunities that exists in Africa. If Goldmans can come up with a 50 year strategy for China, surely other banks can afford to give Africa the same grace period! Tasma

Fascinating perspective on the exits. There's also local intense competition from regional African banks that have sprung up from Morocco, Nigeria, South Africa, and now Kenya.

Thanks so much for writing this! I learnt a lot of things that I had not come across before.

Very good read. Thank you for this 👏🏽👏🏽👏🏽

What a brilliant article. By assesing objectively what made all these big names exiting our market to fail,we shall realize that instead of being a fatality,these various exits may be transformed to a great opportunity which if properly leveraged on will definitely permit Africa to have its say not only on the local financial landscape but also at a global level. All we need is believing in ourselves and on our way of perceiving the world.

This is an interesting and refreshing take on the stance of international banks and their brand promises. Also, very important for us Africans to start looking at ourselves and each other to build solutions that address our challenges in a meaningful way. Thank you Muloongo!

Interesting read Muloongo.